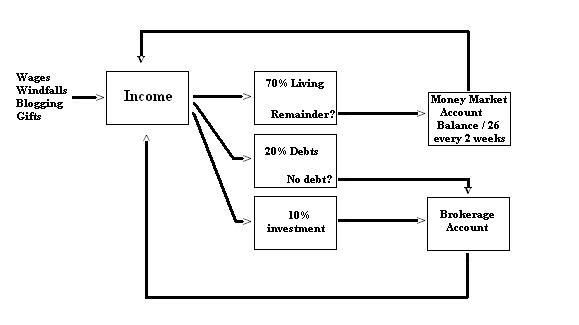

I acknowledged in that post that there are those out there who literally do not have those little bits left over in their budgets. I know you're out there.

I have a way around that dilemma you can use. This is how I build up my investments with cash I must spend on essentials, which for this example is food and fuel (this is a real example, I do this all the time).

There are a few things you will need for this:

- A checking account

- A debit or credit card (ideally, a card that features cash back in some form)

- An Acorns account (this link will get you a $5 sign-up bonus to get started)

- A Lolli account (this is how you are going to get free Bitcoin)

- Optional, for enhanced earnings later on: A BlockFi account (this is how you earn Bitcoin on your Bitcoin)

Set-Up:

- In your new Acorns account, link up your checking account and the credit and/or debit card you make regular purchases with (you can link multiple cards)

- Install the free Acorns browser extension (important: if you use any kind of cookie blocker, turn it off for the Acorns.com site and any merchant site where you shop with the plugin, or when using the Found Money portal on Acorns.com)

- Install the Lolli browser extension (also turn off cookie blocking for the Lolli.com site, the extension itself if prompted, and the merchant website where you are shopping with it)

- The BlockFi account will not require any additional set-up at this time (there is an Acorns offer there that the extension will alert you to though!)

- Shop for necessities!

*quick note about these browser extension links: these are for the Chrome/Brave version, but other browsers are supported, you may have to search separately for the correct extensions; I recommend you check out the Brave browser, you can earn the Basic Attention Token just for using it!

If you dig through the offerings in both Acorns and Lolli, you'll see that most of the options are in the "consumer discretionary" categories: mostly wants, few needs. For a tight budget, this is a deal breaker.

This is where adding the browser extensions comes into play: they will alert you when you are on a website that offers a kickback, and it may be with merchants you would not have expected.

My example from today in this regard: the grocery store I usually make curbside pick-up purchases with.

Food. A basic need.

Here's what I did:

First, I went to my grocer's website, like usual. Only this time, the Lolli app alerted me that they've partnered with my grocer. That means I could get Bitcoin back on this purchase. The alert terms and conditions stated "at least 1% back".

I'm also earning fuel discount points with this grocer, redeemable at Chevron or Texaco stations, and I used a 2% cash back credit card.

Today's purchase came to $38.69. I received:

Food. A basic need.

Here's what I did:

First, I went to my grocer's website, like usual. Only this time, the Lolli app alerted me that they've partnered with my grocer. That means I could get Bitcoin back on this purchase. The alert terms and conditions stated "at least 1% back".

I'm also earning fuel discount points with this grocer, redeemable at Chevron or Texaco stations, and I used a 2% cash back credit card.

Today's purchase came to $38.69. I received:

- $0.77 cents of cash back from my card

- 38 fuel reward points, potentially worth $0.95 cents (more on that later)

- $1.35 worth of Bitcoin (approximately .000041 satoshis at today's BTC price) -- 3.5% back!

So totaling this up, I spent $38.69 on necessities and received kickback benefits of $2.12 (not including the fuel rewards at the moment, the reason why will become clear below), an immediate return of 5.48%!

This is just the start, however.

Depending on what merchant you are spending money with, they may be partnered with either Lolli or Acorns, neither, or sometimes both. You can only use ONE of the programs at a time, so if both offer you something, look each over and activate the option with the greater reward. Don't get greedy here because merchants will only honor one reward program at a time, and possibly will grant neither if they detect you activating multiple offers at once.

This is just the start, however.

Depending on what merchant you are spending money with, they may be partnered with either Lolli or Acorns, neither, or sometimes both. You can only use ONE of the programs at a time, so if both offer you something, look each over and activate the option with the greater reward. Don't get greedy here because merchants will only honor one reward program at a time, and possibly will grant neither if they detect you activating multiple offers at once.

Anyway, I said that this example would also include purchasing fuel, another necessity, so here we go...

I buy fuel for my car and my work trucks at Chevron/Texaco, because in my experience their fuels are superior products to that of their competitors, and because they offer a bonus investment for Acorns account holders: spend at least $20 on an Acorns-linked card at the pump and you'll get a .25 cent bonus investment.

Right now, the best-priced Chevron station near me is selling 87 octane unleaded at $2.57/gallon. To buy $20 worth, I would purchase 7.78 gallons (roughly).

However, I have fuel discount rewards from my grocer of 3.8 cents/gallon from my example purchase (the actual terms are 1 fuel reward of .10 cents/gallon per $100 spent with my grocer, so these numbers are hypothetical, just to demonstrate how this all works based on this one grocery purchase I made today). The discount per gallon is available up to 25 gallons per redemption, but to this example within the context of a smaller budget, I will detail this with a fuel purchase just large enough to get the Acorns bonus.

Because this lowers the price I pay at the pump before fuel is dispensed, it gets me a little more fuel for $20: 7.89 gallons (and that gets me a bit further down the road for the same amount of money...).

I'm again using my 2% cash back card.

So, with the purchase now complete, I have spent $58.69 on necessities and received:

I buy fuel for my car and my work trucks at Chevron/Texaco, because in my experience their fuels are superior products to that of their competitors, and because they offer a bonus investment for Acorns account holders: spend at least $20 on an Acorns-linked card at the pump and you'll get a .25 cent bonus investment.

Right now, the best-priced Chevron station near me is selling 87 octane unleaded at $2.57/gallon. To buy $20 worth, I would purchase 7.78 gallons (roughly).

However, I have fuel discount rewards from my grocer of 3.8 cents/gallon from my example purchase (the actual terms are 1 fuel reward of .10 cents/gallon per $100 spent with my grocer, so these numbers are hypothetical, just to demonstrate how this all works based on this one grocery purchase I made today). The discount per gallon is available up to 25 gallons per redemption, but to this example within the context of a smaller budget, I will detail this with a fuel purchase just large enough to get the Acorns bonus.

Because this lowers the price I pay at the pump before fuel is dispensed, it gets me a little more fuel for $20: 7.89 gallons (and that gets me a bit further down the road for the same amount of money...).

I'm again using my 2% cash back card.

So, with the purchase now complete, I have spent $58.69 on necessities and received:

- $0.77 cents of cash back from my card for the groceries

- 38 fuel reward points

- $1.35 worth of Bitcoin (approximately .000041 satoshis at today's BTC price) for the groceries

- $0.40 cents of cash back for the fuel

- $0.28 cents of additional fuel (difference of available gallons @ $20 with/without rewards discount @ $2.57/gallon

- $0.25 deposited by Chevron into my Acorns account

That makes for an all-in kickback total of $3.05 on $58.69 spent on necessities, for a final return of 5.2%. All without a penny of additional money out of my budget!

So that's then $1.35 of Bitcoin in the Lolli "wallet" and .25 cents invested into my Acorns account directly, leaving the $1.17 of cash back not invested (a total of $2.77; the other .28 cents of kickback value is in your gas tank). When my card's statement closes and that cash becomes accessible, I can either apply it to the statement balance for an effective discount of 2% on my purchases, or since it's "free money" at my disposal that is not a part of my budget, I'm free to plug it into my investments (one good use for cash back: since your Acorns account will draw "round-ups" from your checking account, unless you turn them off, let your cash back cover rounds-ups in part or in full).

So that's then $1.35 of Bitcoin in the Lolli "wallet" and .25 cents invested into my Acorns account directly, leaving the $1.17 of cash back not invested (a total of $2.77; the other .28 cents of kickback value is in your gas tank). When my card's statement closes and that cash becomes accessible, I can either apply it to the statement balance for an effective discount of 2% on my purchases, or since it's "free money" at my disposal that is not a part of my budget, I'm free to plug it into my investments (one good use for cash back: since your Acorns account will draw "round-ups" from your checking account, unless you turn them off, let your cash back cover rounds-ups in part or in full).

(Again, the fuel rewards terms are that 1 reward of .10 cents/gallon becomes available for each $100 of qualifying grocery purchases, so in practice this has to be taken into account in the actual workings of this spending approach. However, because it is valid on up to 25 gallons of fuel per transaction per my grocer's program, if you invest in a few gas cans like I have, then the kickback return on the total outlay assuming $100 spent on groceries and 25 discounted gallons of fuel purchased at $2.47/gallon actually pushes the rate of return to 5.86%, $9.49 of total rewards/discounts received on $161.75 spent.)

Final boost to the whole thing: once you have $15 worth of Bitcoin in your Lolli wallet, you can withdraw it to another Bitcoin wallet elsewhere. This is where BlockFi comes in: I store part of my Bitcoin hodl (Bitcoin lingo for your stash) there where it presently earns 6% annually, paid in Bitcoin. Not only am I getting free Bitcoin by buying my wants and needs, but my collection of satoshis is growing passively, too.

Times are rough right now for a lot of people, no denying that. What I'm hoping to do here is show everyone, whatever their current situation, that there are ways to drum up those powerful little bits with spending you have to do anyway and put them to work building you a better tomorrow. This is but one way I do it, and there are tweaks out there to make what I've shown you here generate even better returns (I wanted to keep it relatively simple today).

The referral links you need to set this up, several of which will give you bonuses to start:

- Create an Acorns account with this link, get $5

- Create a Lolli account with this link, get bonuses for referring others

- Get the Acorns browser extension (this is the Chrome/Brave version, other browsers are supported)

- Get the Lolli browser extension (Chrome/Brave version)

- Create a BlockFi account with this link, various bonus programs available